Previously: Curve-fitting examples...¶

- Consider 1d case (e.g. D=1)

- Given a set of observations $x_1, \dots, x_N$

- and corresponding target values $t_1, \dots, t_N$

- We want to learn a function $y(x, {w}) \approx t$ to predict future values.

$$ y(x, {w}) = w_0 + w_1 x + w_2 x^2 + \dots w_M x^M = \sum_{k=0}^M w_k x^k $$

0th Order Polynomial¶

coeffs = np.polyfit(x, y, 0)

poly = np.poly1d(coeffs)

plt.plot(xx, yy, "g--")

plt.plot(x, y, "ro")

_=plt.plot(xx, poly(xx), "b-")

3rd Order Polynomial¶

coeffs = np.polyfit(x, y, 3)

poly = np.poly1d(coeffs)

plt.plot(xx, yy, "g--")

plt.plot(x, y, "ro")

_=plt.plot(xx, poly(xx), "b-")

12th Order Polynomial¶

coeffs = np.polyfit(x, y, 12)

poly = np.poly1d(coeffs)

plt.plot(xx, yy, "g--")

plt.plot(x, y, "ro")

_=plt.plot(xx, poly(xx), "b-")

Overfitting¶

Root-Mean-Square (RMS) Error: $E_{RMS} = \sqrt{2E(w^*) / N} = \sqrt{\frac{1}{N}\sum_{i=1}^N[f(x_i)-t_i]^2}$

f = plt.figure()

plt.plot(_ps, _trns, 'bo-', label='Training error')

plt.plot(_ps, _tsts, 'rs-', label='Test error')

plt.legend()

plt.xlabel("Order of polynomial")

_=plt.ylabel("RMSE")

Polynomial Coefficients¶

for _s in _d:

print(_s)

w0 0.72054 -0.12625 -0.03885 -0.08472 w1 -0.20345 1.80812 1.37196 -14.13425 w2 -0.82882 -0.62727 101.81045 w3 0.08765 0.20524 -261.91109 w4 -0.08839 354.91284 w5 0.01775 -290.25054 w6 -0.00115 153.36883 w7 -54.19458 w8 12.94331 w9 -2.06431 w10 0.21074 w11 -0.01246 w12 0.00032

Data Set Size: $N = 15$¶

(12th order polynomial)

x1, y1 = generateData(15, True)

coeffs = np.polyfit(x1, y1, 12)

poly = np.poly1d(coeffs)

_=plt.plot(xx, yy, "g--", x1, y1, "ro", xx, poly(xx), "b-")

Data Set Size: $N = 100$¶

(12th order polynomial)

x2, y2 = generateData(100, True)

coeffs = np.polyfit(x2, y2, 12)

poly = np.poly1d(coeffs)

_=plt.plot(xx, yy, "g--", x2, y2, "ro", xx, poly(xx), "b-")

How do we choose the degree of our polynomial?¶

AKA number of features

Numerically, one of the issues traces back to the "conditioning" of the $\Phi^T\Phi$ matrix.

- Recall $\kappa(A)=|A^{-1}||A|$ as the condition number of $A$, $\kappa(A)$.

- One wants $\kappa(A)$ close to 1 for "numerically stable" solutions for $Ax=b$.

Example: Solve for $x=A^{-1}b$ $$ A=\begin{bmatrix}2\alpha & 1 \\ 1 & \frac{2}{\alpha}\end{bmatrix},\quad b=[1,10^{10}] $$ and we verify if we recover $b$ by doing $b=Ax=AA^{-1}b$.

kA = lambda a: np.linalg.cond([[2*a,1.],[1.,2/a]])

a = 10**np.linspace(1,11,21)

k = [kA(_) for _ in a]

plt.loglog(a, k)

plt.xlabel(r'$\alpha$')

_=plt.ylabel(r'$\kappa(A)$')

fA = lambda a: np.array([[2*a,1.],[1.,2./a]])

sA = lambda a: fA(a).dot(np.linalg.solve(fA(a), [1,1e10]))[0]

a = 10**np.linspace(1,11,21)

s = [sA(_) for _ in a]

plt.semilogx(a, np.ones_like(a), 'r--', label='Expected')

plt.semilogx(a, s, 'b-', label='Numerical')

plt.xlabel(r'$\alpha$')

plt.ylabel(r'First element of $AA^{-1}b$')

_=plt.legend()

Rule of Thumb - I¶

First of all, normalize your data

- For example, Scale to [0,1] using max and min, or Scale using mean and std $$\hat{x}=\frac{x-x_{\min}}{x_{\max}-x_{\min}},\quad\mbox{or}\quad \hat{x}=\frac{x-\mu}{\sigma}$$

- Scale input only, or both input and output, depending on the bias

- If you scaled the output, remember to scale the predicted output back when using your trained model.

- The min/max or mean/std should be computed from the training dataset only

Rule of Thumb - II¶

Keep a tall-and-thin shape of the design matrix $\Phi$ for better conditioning - which means,

- For a small number of datapoints, use a low degree

- Otherwise, the model will overfit!

- As you obtain more data, you can gradually increase the degree

- Add more features to represent more data

- Warning: Your model is still limited by the finite amount of data available.

Or -

- Use regularization to control model complexity.

Regularized Linear Regression¶

Regularized Least Squares¶

- Consider the error function $E_D(w) + \lambda E_W(w)$

- Data term $E_D(w)$

- Regularization term $E_W(w)$

- With the sum-of-squares error function and quadratic regularizer, $$ \widetilde{E}(w) = \frac12 \sum_{n=1}^N (y(x^{(n)}, w) - t^{(n)})^2 + \boxed{\frac{\lambda}{2} \| w \|^2} $$

- This is minimized by $$ w = (\lambda I + \Phi^T \Phi)^{-1} \Phi^T t $$

Regularized Least Squares: Derivation¶

Recall that our objective function is

\begin{align} E(w) &= \frac12 \sum_{n=1}^N (w^T \phi(x^{(n)}) - t^{(n)})^2 + \frac{\lambda}{2} w^T w \\ &= \frac12 w^T \Phi^T \Phi w - w^T \Phi^T t + \frac12 t^T t + \frac{\lambda}{2} w^T w \end{align}

Regularized Least Squares: Derivation¶

Compute gradient and set to zero:

$$ \begin{align} \nabla_w E(w) &= \nabla_w \left[ \frac12 w^T \Phi^T \Phi w - w^T \Phi^T t + \frac12 t^T t + \frac{\lambda}{2} w^T w \right] \\ &= \Phi^T \Phi w - \Phi^T t + \lambda w \\ &= (\Phi^T \Phi + \lambda I) w - \Phi^T t = 0 \end{align} $$

Therefore, we get $\boxed{w_{ML} = (\Phi^T \Phi + \lambda I)^{-1} \Phi^T t}$

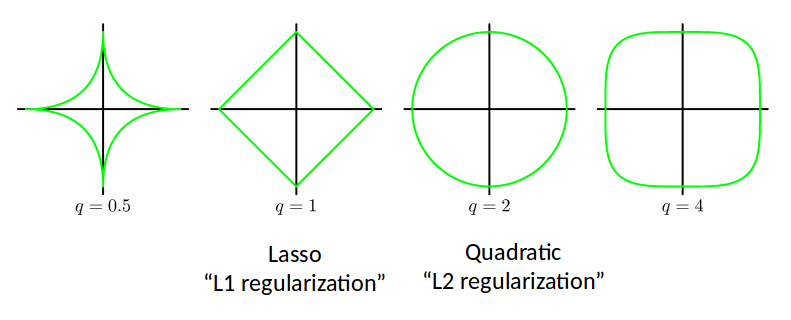

Regularized Least Squares: Norms¶

We can make use of the various $L_p$ norms for different regularizers:

$$ \widetilde{E}(w) = \frac12 \sum_{n=1}^N (w^T \phi(x^{(n)}) - t^{(n)})^2 + \frac{\lambda}{2} \sum_{j=1}^M |w_j|^q $$

L2 regularization is also called Ridge Regression.

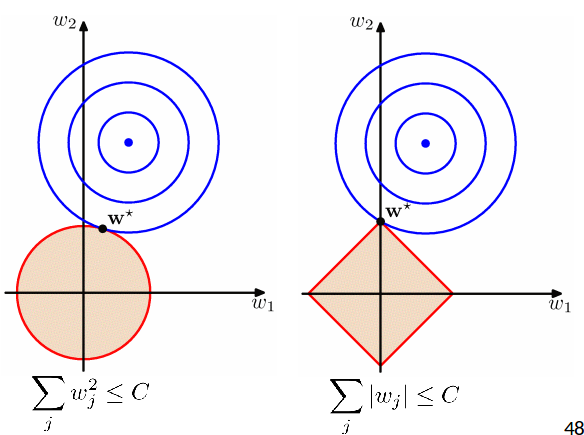

Regularized Least Squares: Comparison¶

- At the solution the contours are always tangent to each other.

- Lasso tends to generate sparser solutions than a quadratic regularizer.

Another explanation for L2 regularization, using Fourier analysis: https://arxiv.org/abs/1806.08734v1

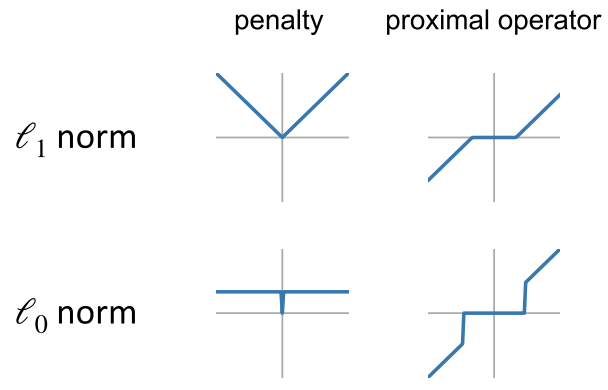

Extra: Solving the L1 case¶

- The L2 regularization $\|w\|_2^2$ is smooth and differentiable, and hence easy to solve.

- But how about the L1 case $\|w\|_1$? The objective is not differentiable whenever one $w_j$ is zero.

Here we briefly discuss the Proximal Gradient Descent (PGD) method to solve this problem.

The algorithm¶

Formally, let's consider $$ \min_w F(w) = h(w) + r(w) $$ where $h(w)$ is differentiable and $r(w)$ is not. In the L1 example,

$$ h(w) = \|\Phi w-t\|^2,\quad r(w) = \lambda \|w\|_1 $$

But here we still assume both $h$ and $r$ are convex.

In short, PGD does the following, $$ w_{k+1} = \text{prox}_{\alpha r}(w_k - \alpha\nabla h(w_k)) $$

- Regular GD for $h$ with a step size $\alpha$

- A special "proximal operator" for $r$

The proximal operator does the following, $$ \text{prox}_{\alpha r}(v) = \arg\min_{u} \frac{1}{2}\|u-v\|^2 + \alpha r(u) $$

- $v$ is the update based on the smooth part of objective

- $u$ is the modification to $v$ considering the non-smooth part

- $u$ is as close to $v$ as possible (1st term), while minimizing $r$ (2nd term)

For typical regularizers, the proximal operators have closed-form solutions.

For example, in the L0 case, we simply zero out values smaller than a threshold.

How it works¶

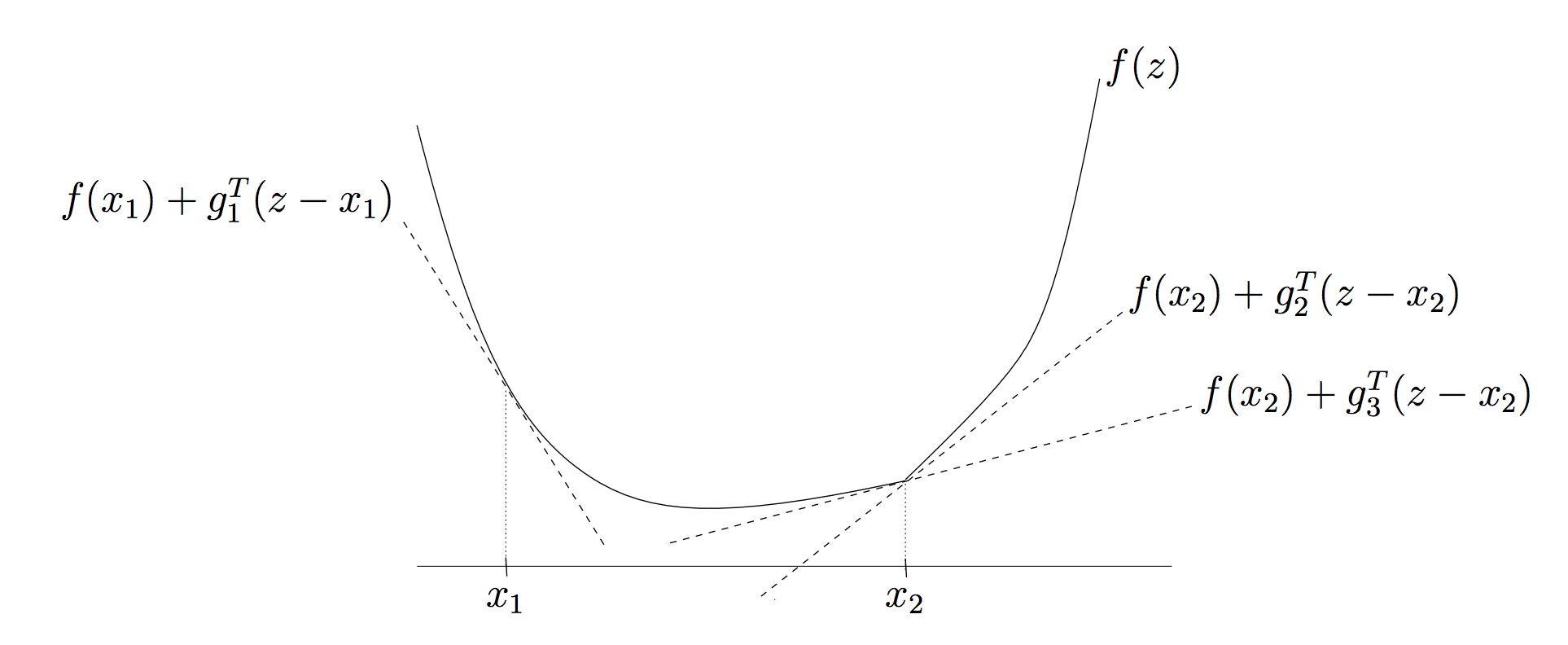

Recall, if the objective were differentiable, e.g., without $r(w)$, the optimality condition is simply $$ \nabla F(w) = \nabla h(w) = 0 $$

From the optimality condition, if we have an iterate $w_k$, the next iterate that we pick satisfies $$ 0 = \nabla h(w_{k+1}) \approx \nabla h(w_k) + \frac{w_{k+1} - w_k}{\alpha} \quad\Rightarrow \quad w_{k+1} = w_k - \alpha \nabla h(w_k) $$

In the non-differentiable case, the optimality condition generalizes to $$ \partial F(w) = \nabla h(w) + \partial r(w)\quad\text{and}\quad 0\in \partial F(w) $$ where $\partial r(w)$ is a special notation called subgradient - a set of vectors $g$ such that for all $v$ $$ r(v) \geq r(w) + g^T (v-w) $$

In analogy to the smooth case, during iterations, we would like $$ 0\in \partial F(w) = \nabla h(w_{k+1}) + \partial r(w_{k+1}) \approx \nabla h(w_k) + \frac{w_{k+1} - w_k}{\alpha} + \partial r(w_{k+1}) $$

If we choose $$ v = w_k - \alpha\nabla h(w_k),\quad u = w_{k+1} $$ then optimality condition is equivalent to $$ 0\in (u-v) + \alpha\partial r(u) $$

But the above is exactly the subgradient in the proximal step: $$ (u-v) + \alpha \partial r(u) = \partial\left( \frac{1}{2}\|u-v\|^2 + \alpha r(u) \right) $$

In other words, the following two are equivalent:

- Evaluating the proximal step

- Satisfying the optimality condition of the original problem (up to the first-order approximation)

Scalar example¶

Next we take a scalar L1 case as an example, so $\|w\|_1=|w|$, and let $w^*$ be a constant, $$ \min_w \frac{1}{2}(w-w^*)^2 + \lambda |w| $$

If $\lambda=0$, the solution is apparently $w=w^*$.

We want $$ 0\in w-w^* + \lambda \partial |w| $$

If $w>0$, then $\partial |w|=\nabla w=1$, and the equation simplifies $$ 0 = w-w^* + \lambda \Rightarrow w = w^* - \lambda $$

But this relation requires $w>0$, or $w^* > \lambda$.

So, when $w^* > \lambda$, the solution is $w = w^* - \lambda$.

If $w<0$, similarly, we would get: when $w^* < -\lambda$, the solution is $w = w^* + \lambda$.

If $w=0$, then $\partial |w|=[-1,1]$, and $$ 0\in w-w^* + \lambda [-1, 1] = -w^* + [-\lambda, \lambda]\quad \text{or}\quad w^* \in [-\lambda, \lambda] $$ This means, when $|w^*|\leq \lambda$, we simply zero out $w=0$ - this is where the sparsity comes in.

The above recovers the L1 proximal operator.

Some notes¶

- More information on proximal gradient method wiki and an introductory text

Examples: Regularized regression¶

Ridge Regression¶

rdg_sc, rdg_coef = fitModel(1.0, lm.Ridge)

Lasso¶

las_sc, las_coef = fitModel(0.01, lm.Lasso)

LR vs Ridge vs Lasso¶

ii = np.arange(13)

f = plt.figure(figsize=(6,4))

plt.semilogy(ii, np.abs(_cs[11]), 'r--', label='LR')

plt.semilogy(ii, np.abs(rdg_coef), 'b-', label='Ridge')

plt.semilogy(ii, np.abs(las_coef), 'g-', label='Lasso')

plt.legend()

_=plt.xlabel(r'$w_i$')

Bad choice of hyperparameter¶

_, _ = fitModel(1e-8, lm.Ridge)

_, _ = fitModel(1e8, lm.Ridge)

Choosing the best hyperparameter¶

f = plt.figure()

plt.plot(np.log(lams), errs[0], 'b-', label='Training error')

plt.plot(np.log(lams), errs[1], 'r-', label='Test error')

plt.xlabel(r'$\log(\lambda)$')

_=plt.ylabel('1-R2')

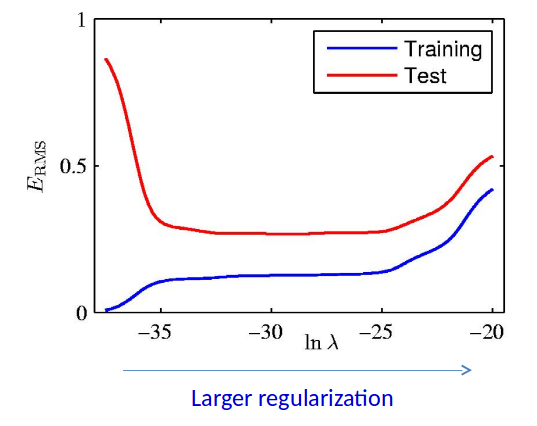

Ridge Regularization: $E_{RMS}$ vs $\ln\lambda$¶

NOTE: For simplicity of presentation, we divided the data into training set and test set. However, it’s not legitimate to find the optimal hyperparameter based on the test set. We will talk about legitimate ways of doing this when we cover model selection and cross-validation.

Regularized Least Squares: Summary¶

- Simple modification of linear regression

- L2 Regularization controls the tradeoff between fitting error and complexity.

- Small L2 regularization results in complex models, but with risk of overfitting

- Large L2 regularization results in simple models, but with risk of underfitting

- It is important to find an optimal regularization that balances between the two

- More on model selection in future lectures

One more model... Elastic net¶

- Combination of Ridge and Lasso $$ \widetilde{E}(w) = \frac12 \sum_{n=1}^N (w^T \phi(x^{(n)}) - t^{(n)})^2 + \lambda\left( \frac{1-\alpha}{2} \sum_{j=1}^M |w_j|^2 + \alpha\sum_{j=1}^M |w_j| \right) $$

- Works better when the features are correlated.

- More details:

- [MLaPP] Chp. 13.5.3

- H. Zou and T. Hastie, Regularization and variable selection via the elastic net, 2005

Yet more models...¶

The bias of the Lasso estimate for a truly nonzero variable is about $\lambda$ for large regression coefficients coefficients.

To fix the issue: Adaptive Lasso, MCP, SCAD

- for those who are interested: https://myweb.uiowa.edu/pbreheny/7600/s16/notes/2-29.pdf

When it comes to deep learning¶

We will see Double-Descent phenomenon - Errors in training and test both decrease as number of features increase.

To be discussed more later in this module.